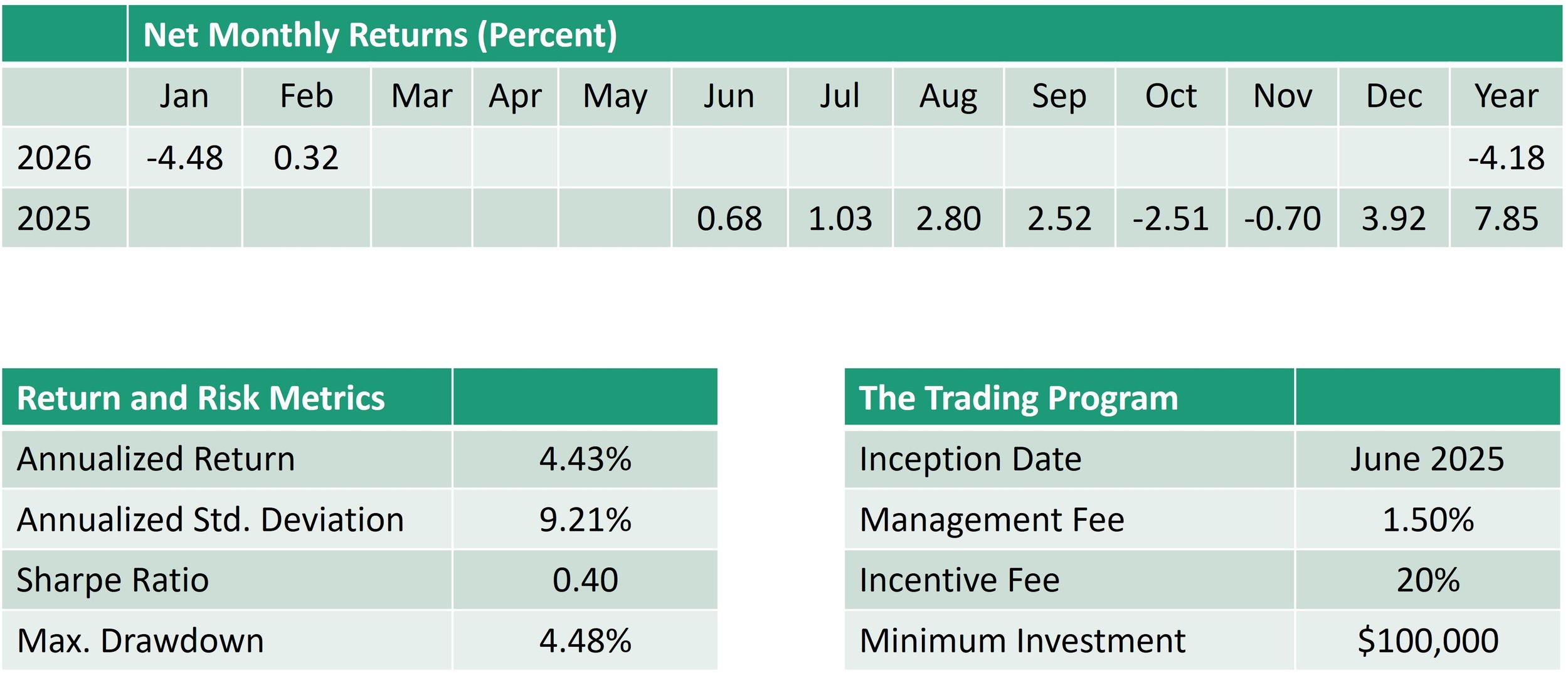

February 2026

In February, the Volatility Long/Short trading program gained 0.32 percent after fees. It was a challenging period. The portfolio had about as many winning as losing days. The main contributor to gains was short call positions on E-mini S&P 500 futures contracts. This returned approximately 0.25 percent. Positions in VIX futures contracts, meanwhile, were relatively flat.

During the month, market anxiety appeared to be slowly building. Ten-year U.S. Treasury bond futures gained 1.8 percent, and the price of the near-dated VIX futures contract increased from 17.9 to 20.6. The S&P 500 equity index moved from positive to negative territory before ending the month down 1.6 percent. Daily equity declines were large enough to result in some daily losses on VIX futures positions. However, they were not extreme enough to generate the portfolio gains associated with equity market crashes.